Indebtedness

A credible and sustainable mobilization The country intends to increase its external fundraising capacity to 45% of GDP by 2023.

Planning

The main development priorities Large-scale sporting events, priority projects for the reconstruction of the North-West and South-West regions constitute the

Campaign NEFC

The NEFC popularizes its computer platform The launching took place on 25 August 2020 in Yaoundé in front of the

PRESS KIT THE COMPUTER PLATFORM OF THE NATIONAL ECONOMIC AND FINANCIAL COMMITTEE

Download the press kit

Performance

A tool for securing financial transactions The NEFC’s IT platform is one of the best ways to track and control

Budget 2021-2023

Controlled trajectory for a return to growth For the next three years, the government is counting on projected growth of

Presentation of the National Sinking Fund

The Sinking Fund of Cameroon (CAA) is a public establishment created by Decree No. 85/1176 of 28 August 1985. It

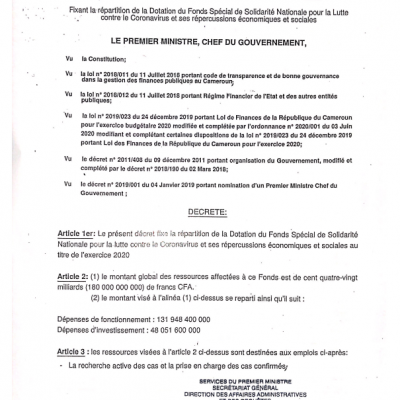

Decree N° 2020/3221/PM of 22 JUL 2020

To fix the allocation of the Endownment of the Special National Solidarity Fund for the Fight against Coronavirus and its

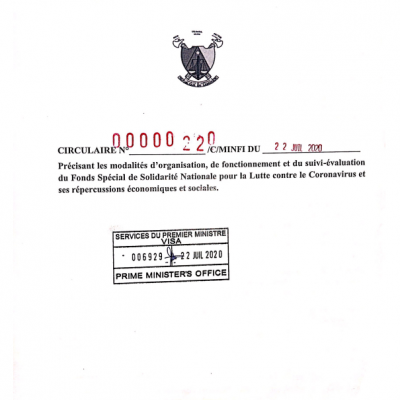

Circular n° 00000220/C/MINFI of 22 jul 2020

Specifying the modalities of organization, operation and monitoring-evaluation of the Special National Solidarity Fund for the Fight against Coronavirus and

Radio-presse release of July 17, 2020 relating to the continuation of the clearance of the State debt

Radio-presse release N°20/00004645/CRP/MINFI/SG/DGB/DPB/CCC/CEA1 of July 17, 2020 relating to the continuation of the clearance of the State debt. Download Radio-Press